Where to Get Continued 10 Return

RiverNorthPhotography/iStock Unreleased via Getty Images

Fundamental 10-Step Analysis of Berkshire Hathaway Health & Valuation

Berkshire Hathaway (NYSE:BRK.B)(NYSE:BRK.A) is a diversified conglomerate holding company based out of Omaha, Nebraska run by...well I think you get the idea! Let's jump right in - in the 2020 Annual Letter published by Warren Buffett in February 2021 he states Berkshire has four crown jewels: 1) The insurance businesses and their combined over $138B in "float" used for investing purposes, 2) The wholly-owned subsidiary of Burlington Northern Santa Fe (BNSF) which is America's largest railroad by freight volume, 3) The 5.4% ownership of Apple (AAPL) which is worth $126.7B as of today, and 4) The wholly-owned subsidiary of Berkshire Hathaway energy which alone has annual earnings of $3.4B.

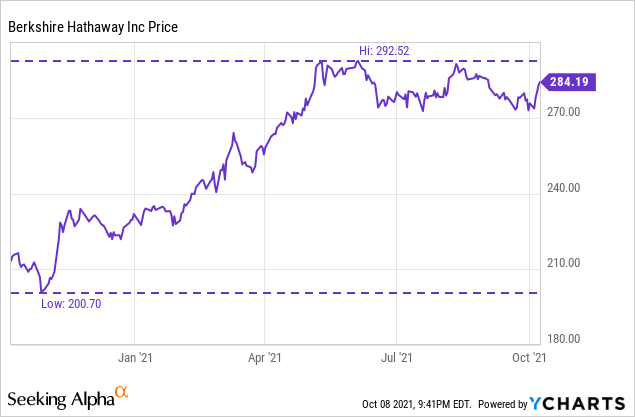

Despite moving up quickly from the late October 2020 lows of $200/share to nearly $300 in June, Berkshire has traded sideways since May of this year.

With many bemoaning the ~$140B cash balance and underperformance versus the S&P 500 ovr the past 5 years, Berkshire has become known as a safe haven during economic uncertainties - and with the run-up in the markets, coupled with rising yields and political uncertainty - I believe Berkshire presents a fantastic opportunity for analysis as presently valued at $643.26B.

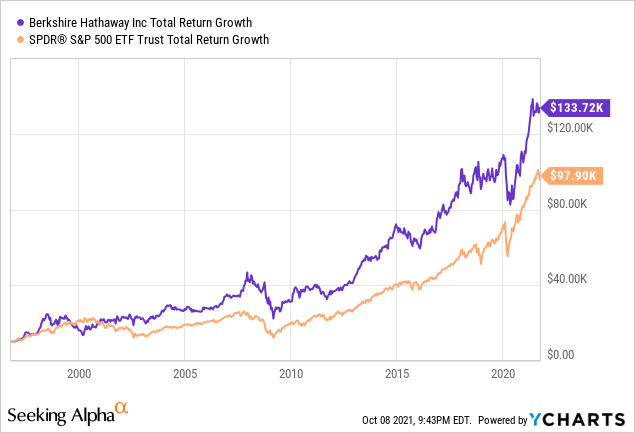

Just look at this chart from October 1996 to present, a period of 35 years, showing the price growth of $10,000 by Berkshire Hathaway and the S&P 500. Berkshire, through wise investments, sensible acquisitions, and insurance float compounding, was able to beat the S&P 500 by 35% during the time period. While the value story is well known, it is the continued revenue growth and most importantly the share buybacks that present a fantastic future for the company. This is additionally coupled with the high return on invested capital presented by Apple as well as the increased dividend potential it has which directly benefits Berkshire - at over 887.135MM shares held worth $126.77B, the Apple investment alone represents just under 20% of Berkshire's market cap.

Using a 10-Step Fundamental Analysis detailed here, I will go through 10 important components of Berkshire Hathaway and how it measures up on each metric, either assigning a 1/1, 0.5/1 or a 0/1 for each.

Strong Revenue & Income Growth Considering The "Law of Big Numbers"

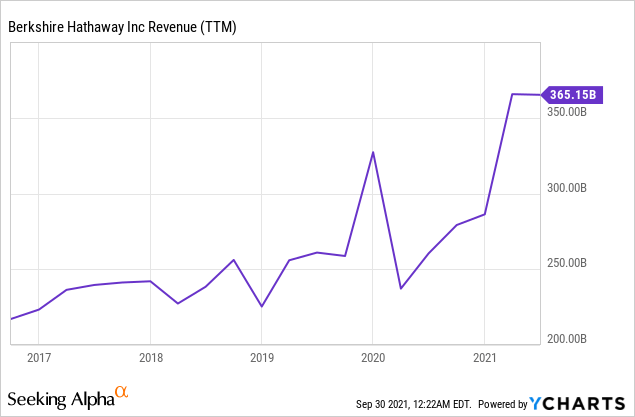

Looking at trailing 12-month numbers as of June 30, 2021 for operating revenue over the past 5 years, Berkshire has increased from $217.35B to $365.15B. Now, these numbers come with a significant asterisk to it due to Berkshire's equities portfolio that is $291B and generated $104B towards revenue in the form of gains. Therefore, this revenue should not be used as the basis for determining operating revenue, which has increased from $217.226B to $261.118B in the trailing twelve months over the past 5 years. Revenue increase has come from a combination of insurance growth, BNSF growth, and Berkshire Hathaway Energy's growth primarily. This operating revenue growth has grown at 3.75% CAGR over the past 5 years, but taking into account the share buybacks creates an even more enhanced piece of data: per-share revenue - which grew from $88.14/share to $115.48/share or 5.57% CAGR. This is the effect of share buybacks and how they can even further enhance growth for the investor.

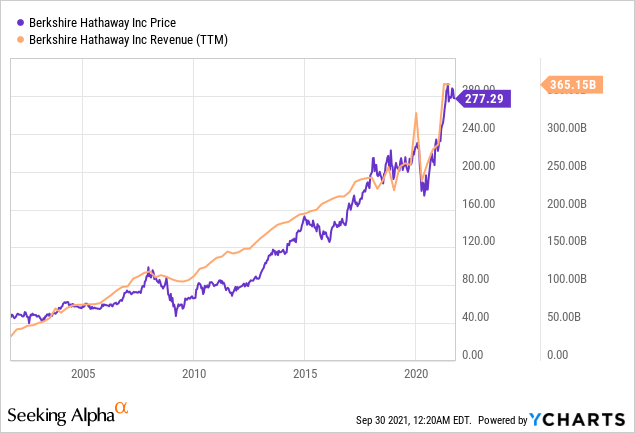

Notice the effects of GAAP accounting on the revenue for Berkshire Hathaway during the pandemic crash of 2020 - revenue declined nearly $100B in one quarter due to the equity crash. Outside of this, it is very clear that Berkshire's revenue and price tend to follow very closely with one another as the effects of operating revenue performance and equity portfolio performance mirror Berkshire's equity price itself.

While 5.57% per share CAGR on operating revenue isn't a number that inspires confidence in double-digit growth in the years to come, it is a very strong growth rate for such a large company with such well-established businesses. As my projections show below, I am anticipating similar 4-5% revenue growth in the years to come based primarily on inflation price growth, commodity demand increases, and strong energy performance within Berkshire Hathaway Energy.

Revenue Growth: $217.35B -> $365.15B over 5 years, 13% per share CAGR / OpRev: 5.57% per share CAGR

Pay more attention to the operating revenue growing by 5.57% per share CAGR, not the revenue growth including equity portfolio performance. Score: 1/1

Although net income is not inherently as insightful of a valuation metric compared to free cash flow, Berkshire's net income is truly a difficult factor to rely upon when seeking actual results of the business itself. As Warren Buffet described in the 2018 annual letter:

"Our advice? Focus on operating earnings, paying little attention to gains or losses of any variety. My saying that in no way diminishes the importance of our investments to Berkshire. Over time, Charlie and I expect them to deliver substantial gains, albeit with highly irregular timing." (Source)

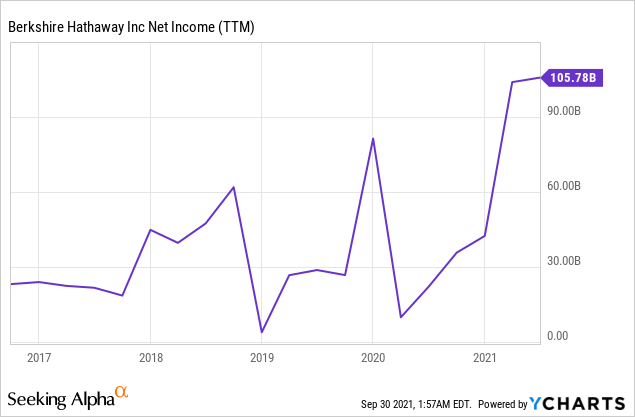

Using trailing twelve-month figures as of June 30, 2021 - Berkshire Hathaway net income has grown from $25.495B to $110.777B in the past 5 years representing a 34% CAGR. However, let's look at the actual operating earnings to see how the operating businesses themselves are doing for a more reflective look at Berkshire - net income from the operating results has grown from $17.568B to $24.203B in the past 5 years for a 6.62% CAGR. These figures are further enhanced when seen through a per-share basis to account for the buybacks: $7.12/share in earnings growing to $10.71/share in earnings over 5 years or an 8.37% CAGR. This is a strong growth rate for a mature business especially in a twelve-month period where two quarters are in 2020.

Looking towards the future there are two major headwinds that Berkshire Hathaway will face in terms of both revenue and income growth: 1) Will the law of big numbers with mostly mature businesses continue to deteriorate growth percentages going forward? and 2) Can Berkshire find a use for the roughly $70-$80B in cash that is not required for insurance reserves to meaningfully impact earnings long into the future? It seems clear to me that two of Berkshire's crown jewels, the BNSF railroad, and Berkshire Hathaway Energy, have long runways ahead of them for growth - especially the energy company. The third jewel of insurance is mixed: as vehicles continue becoming safer and increasingly more expensive, insurance premiums will rise and payouts may decrease, but the self-driving component may mean less insurance coverage is required over time by regulatory agencies or by consumer preference - though there is no evidence suggesting either headwind is coming to fruition as of present.

Income Growth: $25.495B -> $110.777B over 5 years, 34% CAGR / OpIncome 8.57% per share CAGR

Income growth is stronger than revenue growth reflecting excellent margin control and businesses with economic moats as Buffett prefers, further enhanced by strong share buybacks in recent quarters. Score: 1/1

The Fabled "Fortress" Balance Sheet, Though With Increasing Debt...

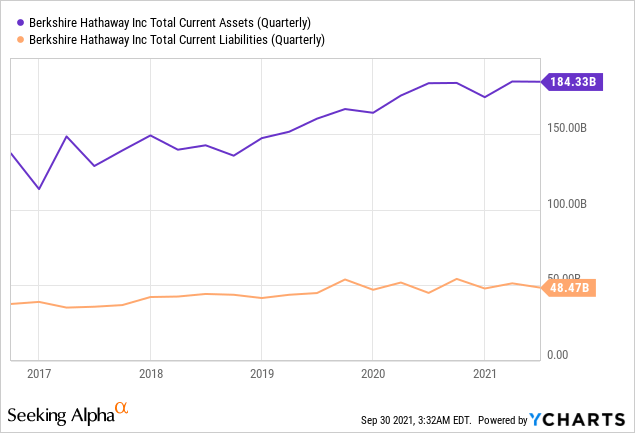

Due to the fact that Berkshire has substantial insurance operations that allow for "float" in the form of current assets, this ratio is shown very favorably for the company. $184.33B in current assets versus $48.47B in current liabilities shows a business that has over $135B more current assets than current liabilities, a ratio that only banks, insurers, and a select few technology companies have. This is made even more impressive by the fact that most railroads (including every major US & Canadian railroad other than Kansas City Southern) have greater current liabilities than current assets due to the nature of the business.

I believe the pandemic has only increased Berkshire's desire to have a "fortress" balance sheet, one where current assets dwarf current liabilities, with the only exception in the future being an acquisition that meaningfully fits into the ecosystem and temporarily uses current assets towards said acquisition.

Assets v Liabilities : $184.33B current assets v. $48.47B current liabilities / normal for ins but growing

While common for insurance companies, current assets do exceed current liabilities by over $135B, representing fantastic liquidity. Capital-intensive operating businesses in the mix make this even more impressive. Score: 1/1

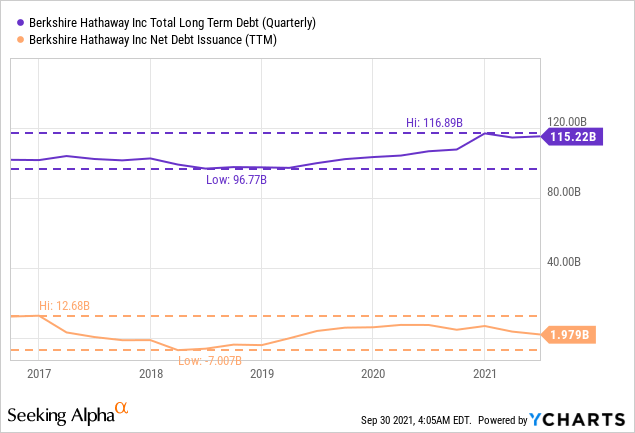

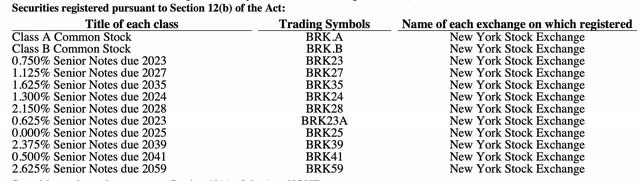

While $115B in long term debt is a very large figure by almost any company's standards, for Berkshire it represents less than 4 times current free cash flow, $70B less than the current assets of the business, and is being issued at very low rates even by today's standards of incredibly low rates. In fact, just look at the debt issuance in Berkshire's 2020 10-K...

https://berkshirehathaway.com/2020ar/202010-k.pdf

Berkshire Hathaway 2020 10-K

Some of these notes are issued at 0% and the highest is 2.625% until 2059 - or 38 years from now! Most of these notes are lower than the historical inflation rate meaning that Berkshire in most cases is being paid to borrow this money once inflation is taken into account - especially when taking into account the company's return on invested capital which we will dive into next.

While the trend for many major corporations during the pandemic has been to issue increasing amounts of debt, I believe Berkshire will not exceed 5 times free cash flow on a go-forward basis.

Long Term Debt: Large Number BUT Less Than 4x FCF, Issued at Low Rates & Deployed Wisely

While the overall number is very large, Management is prudently using debt, it is less than 4 times free cash flow and is issued at rates that are significantly below inflation - and deployed wisely. Score: 1/1

The Main Story: Consistent Return on Capital & The Ever-Increasing Share Buyback Factor

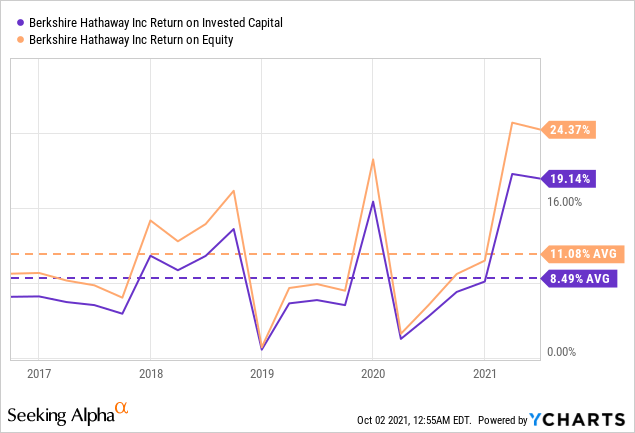

Capital deployment is somewhat of a specialty it would seem to Buffett and Munger so I was surprised by their overall standard levels of return both based on invested capital and equity. Return on invested capital is perhaps one of the greatest indicators of a competent management team - how they invest and allocate capital into the business. The average of all S&P 500 companies is approximately 7%. Looking at doing better than average and towards companies deploying their money into high-quality investments, I look for businesses earning more than 10% return on invested capital. Return on invested capital is a financial metric favored by Charlie Munger, stating "It's obvious that if a company generates high returns on capital and reinvests at high returns, it will do well." (Source)

With an average ROIC of 8.49% over the past 5 years, Berkshire falls short of the 10% benchmark and barely outpaces the market average. Now let's dig a bit deeper to see why: 1) The current percentage is 19.14% and the number can swing wildly from quarter to quarter because of the equity investments and their mark to market effect on the bottom line. Essentially, a bad quarter in the market means a lower net income (though not necessarily a lower operating income), which skews the percentage much lower; and 2) The cash reserves Buffett likes to keep on hand in the $70B range and the majority of the cash position is held in government bonds and Treasury bills, which though secure do return very little and thus further skew the number lower. The first is a strong factor in artificially lowering and raising ROIC and Return on Equity, while the second is a management choice that is somewhat of a necessity due to the unforeseen liquidity demands of the insurance business.

Invested Capital & Equity Returns: 8.49% ROIC avg 5 years + Current 19% / 11% ROE avg 5 + Current 24%

I struggled with going 1/1 vs 0.5/1 and ultimately believe it is somewhere in between, though slightly closer to 1/1. The 5-year average ROE is strong for such a large company and is very strong presently; whereas the ROIC is weaker for the 5-year average (though that is partially due to the insurance reserves dragging the investment average down). Overall, for such a large cash position, these numbers are strong. Score: 1/1

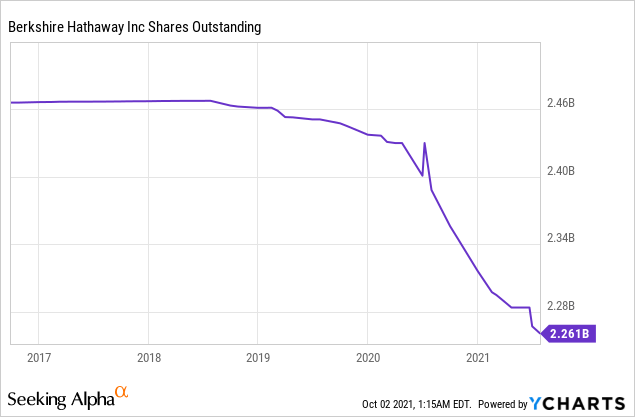

For years Berkshire did not allocate capital through share repurchases and actually issued shares for important transactions that took place such as the acquisition of General Re in the late 1990s and BNSF in 2010. Shares outstanding within the company and the way management either enhances shareholder value or dilutes it through buybacks or share issuances is a very meaningful metric for overall investor return. While some companies will buy back 1% of shares annually and have a very good buyback program at that, others will dilute and raise capital through issuing new shares. With Berkshire, the buyback program which began in vigor in 2019 is truly a shift in capital allocation for the company - and some see it as admitting Buffett and Munger's decreased ability to effectively allocate so much capital. In 5 years, the shares outstanding have decreased from 2.466B to 2.261B, representing an 8.39% decrease in shares. But it's the last 12 months that have truly been impressive: 2.38B to 2.261B or a 5.32% reduction in shares - truly a remarkable number for such a large-cap company.

Berkshire is showing that buybacks are one of the best ways to enhance shareholder returns in a tax-efficient manner in the long term. The growth of the earnings power is magnified by the decrease in the share count, creating a compounding machine. As Buffett mentions in the 2020 annual report, "The math of repurchases grinds away slowly, but can be powerful over time. The process offers a simple way for investors to own an ever-expanding portion of exceptional businesses."

As shown in my projections going forward and based on the past 4 quarters of buybacks, I believe Berkshire will continue buying back shares at a rate of 4-5% annually unless the book valuation of Berkshire begins expanding beyond 1.4x, at which point I believe Buffett will scale back buybacks.

Buybacks: 2.466B -> 2.261B shares over 5 years, 8.39% reduction / 5.32% reduction in 12 months!

Shares have decreased over the past 5 years and have rapidly accelerated in the past 12 months especially. Score: 1/1

Management purposefully does not issue a dividend of any kind, preferring to return capital to shareholders through share buybacks and through reinvestment into the business at high rates of return. These two metrics together offer investors a far more lucrative rate of return due to the effects of internal compounding and the tax efficiency of buybacks for shareholder benefit.

Dividend : $0 dividend annual, 0% fwd yield / Management prefers other means of return

The no dividend policy is supported by outstanding return by other means. In this case, the policy works well. Therefore, less is more. Score: 1/1

Strong & Growing Free Cash Flow At A Fair Valuation

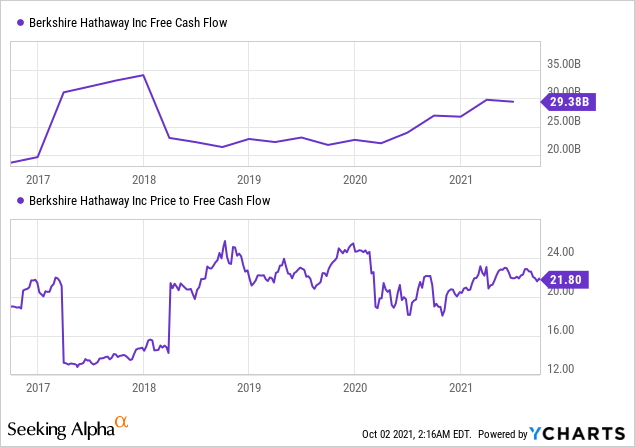

From the standpoint of a company's operational strength and long-term stability, free cash flow represents a very meaningful metric and the primary factor I look towards when creating a valuation metric and measuring long-term stability and growth. Berkshire has grown free cash flow from $17.42B to $29.38B in the past 5 years representing an 11.02% CAGR. For such a large company spending so significantly annually on capital expenditures, this growth is quite impressive and is further enhanced when noting it on a per-share basis due to the buybacks during the prior 2 years - $7.06/share to $13/share or a 13% AGR.

Free Cash Flow: $17.42B -> $29.38B in 5 yr (11% CAGR increase) / 13% CAGR on a per share basis

Free cash growth over the past 5 years is growing considerably and heightens the likelihood of continued share buybacks for investors. Score: 1/1

Now for the component of valuation with regards to Berkshire Hathaway: First let's look at the simplest method, free cash flow. Berkshire Hathaway, based on the $643.26B market cap, is selling for 21.89 times free cash flow for the trailing twelve months - representing a 4.57% initial rate of return based on free cash flow with an 11% CAGR free cash flow growth over the past 5 years. That being said, the company does have an extra $70B in cash on the books beyond the $70B Buffett requires for insurance reserves - if we subtract that off of the books for a $573.26B market cap - it comes in at 19.51 times free cash flow representing a 5.13% initial rate of return with an 11% CAGR growth.

By my standard metrics of looking for growth companies selling for under 20 times free cash flow, the valuation of Berkshire is borderline. Purely on a market cap valuation, it is priced above my metric, but subtracting out cash it is slightly below it.

Valuation: 21.89x FCF; 4.57% implied initial return w/ 11% CAGR free cash flow

I'm sticking to the methodology here and being straightforward: Berkshire is not a high-growth company and seems slightly overpriced based on this metric - BUT I encourage you to continue reading to see why I believe there are other valuation methods that may be better than this one in this instance. Score: 0.5/1

Overall Berkshire Hathaway Recap & Valuation

Let's examine valuation in multiple ways since the company itself is extremely complex and offers a number of different ways to value it.

First, let's look at it from the standpoint of book valuation since Buffett himself has previously used this valuation methodology for Berkshire. Taking a series of assumptions: book value growth of 5.5% (half of the previous 5-year rate of 11%) with a terminal valuation of 1.3x book value and continued 4% share count reduction annually puts the valuation at $675 per share in 10 years for a roughly 9.3% CAGR.

Second, a variation of this assuming no further buybacks but the continued growth of book value: book value growth of 11% (in line with previous 5-year rate), terminal valuation of just 1.2x book value, and NO further share buybacks puts the valuation at $700 per share in 10 years for a roughly 9.7% CAGR.

A third and final book value variation with a mix of increased book value growth and share buybacks: book value growth of 7.5%, terminal valuation of 1.2x book value and continued 4% share count reduction annually puts the valuation at $774 per share in 10 years for a roughly 10.8% CAGR .

Let's take a series of assumptions based on free cash flow: 5.5% annual free cash flow growth (half the previous 5-year average), 4% annual share reduction, and a valuation of 20 times earnings (below 5-year average). What does this give investors in terms of returns over the next 10 years?

Roughly a 9.2% annual return for Berkshire Hathaway based on the share price. This lines up nicely with the above assumption and I believe it is safe to say with continued share buybacks, strong continued operational performance, and a growing book value Berkshire will return between 9-10% annually in a manner befitting conservative investors looking for the safety of a core holding in the portfolio.

Please see this blog post here to understand the methodology behind the 10-step analysis.

Revenue Growth: $217.35B -> $365.15B over 5 years, 13% per share CAGR // OpRev: 5.57% per share CAGR Income Growth: $25.495B -> $110.777B over 5 years, 34% CAGR // OpIncome 8.57% per share CAGR Assets v Liabilities: $184.33B current assets v. $48.47B current liabilities / normal for ins but growing Long Term Debt: Large Number BUT Less Than 4x FCF, Issued at LOW Rates & Deployed Wisely Invested Capital & Equity Returns: 8.49% ROIC avg 5 years + Current 19% / 11% ROE avg 5 + Current 24% Buybacks: 2.466B -> 2.261B shares over 5 years, 8.39% reduction // 5.32% reduction in 12 months! Dividend: $0 dividend annual, 0% fwd yield // Management prefers other means of return Free Cash Flow: $17.42B -> $29.38B in 5 yr (11% CAGR increase) / 13% CAGR on a per share basis Valuation: 21.33x FCF; 4.69% implied initial return w/ 11% CAGR free cash flow Management & Moat: Buffett and Munger Are Obviously Best of Breed Running Compelling Co's Based on 10-Step Analysis: 9.5 out of 10

This article was written by

32-year-old long-term investor, business owner, and hospitality development professional from Orange County, California. I am primarily focused on analyzing high-quality businesses that are simple, predictable, and free cash flow generative with strong economic moats for paying increasing dividends over the long term for continual reinvestment. The goal is to analyze, identify, and have a level of competence and confidence in the underlying business and analyze equities as you would a whole business, of which we have the opportunity to own a portion. My strategies are less focused on hitting "home runs", and rather consistently hitting "singles" and "doubles" while allowing compounding to do the heavy lifting over time. My academic background is in political science, art history, and real estate from the University of California, Irvine. Thank you for reading my articles and I always appreciate vibrant comment sections!

Disclosure: I/we have a beneficial long position in the shares of BRK.B either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Source: https://seekingalpha.com/article/4459158-berkshire-hathaway-strong-buybacks-continued-compounding-10-percent-returns-annually

{kind=link}

Post a Comment for "Where to Get Continued 10 Return"